While some hospitals are paying five to 10 times more for cancer drugs during a monthslong shortage, the U.S. saw 14 new drug supply issues since early August.

Here are 14 new drug shortages, according to data from the FDA and the American Society of Health-System Pharmacists.

Editor’s note: The drugs are listed in alphabetical order.

1. Alfuzosin extended-release tablets: Three solutions are unavailable and two are available, and the shortage is predicted to recover in August. The drug relaxes a patient’s bladder and prostate muscles.

2. Atropine sulfate ophthalmic ointment: Bausch Health is reporting a short-term shortage of the medication that’s used to dilate the pupil before eye exams. The company is the sole supplier of the solution and did not share an estimated release date.

3. Azacitidine injections: Three drugmakers stopped making 100 milligram solutions of the leukemia drug.

4. Collagenase ointments: There is not enough supply for usual ordering of the ointment that’s used to treat burned skin and skin ulcers as Smith & Nephew has two solutions on intermittent back order without a release date.

5. Glipizide XL tablets: Pfizer discontinued manufacturing the Type 2 diabetes drug.

7. Iobenguane I-131 injections: Progenics Pharmaceuticals stopped making two solutions because of low demand for the oncology medication.

8. Iodine and potassium iodide topical solutions: Two solutions of the dermatology drug are in shortage and one solution is available. Cooper Surgical could not estimate a resupply date, and Gordon Laboratories predicted mid-September.

9. Nitroglycerin injections: One solution of the hypertension drug is available as three others are in limited supply without a release date.

10. Nystatin topical powder: Padagis has two solutions of the antifungal medication on allocation through October and one on intermittent back order. No other solutions are available.

11. Pamidronate disodium injections: Five solutions of the drug that treats bone fragility are in shortage. Viatris said it expects two products to return to normal supply levels in September, and Pfizer predicted resupply between October and January for its three solutions.

12. Piroxicam capsules: Pfizer said it is discontinuing production of the painkiller. Supply of the 20 milligram solutions is expected to last until October.

13. Tedizolid injections: As operations wind down at Nabriva Therapeutics and transition to Merck, there’s insufficient supply of the bacterial skin infection drug. Resupply is expected in late August.

14. Theophylline 24-hour extended-release capsules and tablets: Six solutions of the lung disease medication are on back order and two are available. Rhodes Pharmaceuticals could not forecast a resupply date for two of its solutions, and Endo Pharmaceuticals predicted its shortage to end in October.

Hospitals and physicians are paying millions of dollars for a hidden fee to receive reimbursement from payers electronically, ProPublica reported Aug. 15.

Payers and middlemen charge healthcare providers as much as 5 percent to process electronic payments, according to the story. The ACA required payers to offer electronic funds transfers and nudged physicians to take them. CMS at one time prohibited the processing fees before reversing course.

Tim Reiner, senior vice president of revenue management of Altamonte Springs, Fla.-based AdventHealth, complained to CMS about the fees in 2020, the news outlet reported. “I have to pay $1.8M in expenses that I could use on PPE for our employees, or setting up testing sites, or providing charity care, or covering other community benefits,” he wrote.

“It’s ridiculous,” Karen Jackson, a retired senior CMS official, told the news outlet.

The U.S. Department of Veterans of Affairs has declined to pay the fees, declaring them illegal, according to the story.

The pushback against the fees has been led by Alex Shteynshlyuger, MD, a private urologist in New York City, while the campaign to keep them has been spearheaded by Matthew Albright, chief lobbyist at payment processing company Zelis, according to the article. Mr. Albright, a former CMS official, had pressed CMS on getting rid of its ban on the fees. The agency told ProPublica it had no legal authority to outlaw the fees, adding that it “receives feedback from a wide range of stakeholders on an ongoing basis.”

Other electronic payment vendors include UnitedHealth Group subsidiaries Change Healthcare and VPay. UnitedHealth told ProPublica the companies cut down on administrative burden and speed up payments for providers. Zelis told the news outlet that it helps prevent “many of the obstacles that keep providers from efficiently initiating, receiving, and benefitting from electronic payments.”

July 24, 2023 – Pfizer announced immediate efforts to provide relief and repair the damage caused to its manufacturing facility in Rocky Mount, North Carolina after a violent tornado swept through the town on Wednesday, July 19. All 3,200 local Pfizer colleagues reporting to this manufacturing site are safe and accounted for after excellent implementation of the site’s long-standing evacuation plan. Crews are working around-the-clock to restore power, assess the structural integrity of the building and move finished medicines to nearby sites for storage.

Pfizer also announced a donation to the American Red Cross North Carolina Chapter and United Way Tar River Region to support the relief and recovery needs. Additionally, the Pfizer Foundation will match employee donations to these organizations.

The site is closed while the damage is assessed. Pfizer is committed to rapidly restoring full function to the site, which plays a critical role in the U.S. healthcare system. This effort is in close partnership with the U.S. Food and Drug Administration Commissioner Robert Califf, North Carolina Governor Roy Cooper as well as other state, local and federal officials.

Most of the damage was caused to the warehouse facility, which stores raw materials, packaging supplies, and finished medicines awaiting release by quality assurance. Pfizer is working diligently to move product to other nearby sites for storage and to identify sources to replace damaged raw materials and supplies. Pfizer is also exploring alternative manufacturing locations for production across our significant manufacturing presence in the U.S. and internationally and across the company’s partner network. After an initial assessment, there does not appear to be any major damage to the medicine production areas.

Since 1968, the Rocky Mount facility has been a key producer for sterile injectables. Currently, it is responsible for manufacturing nearly 25 percent of all Pfizer’s sterile injectables – including anesthesia, analgesia, therapeutics, anti-infectives and neuromuscular blockers – which is nearly 8 percent of all the sterile injectables used in U.S. hospitals. The site is one of 10 Pfizer manufacturing sites located in the United States.

In the constant search for ways to cut costs across the board, one of the biggest points of debate for IDNs and providers is the decision between domestic or international manufacturing for their supplies. The pandemic illuminated the need for increased manufacturing in the United States as the demand for PPE and other materials skyrocketed. Companies without any onshore manufacturing were much more likely to struggle with sourcing materials for their clients, but the labor and raw material costs make domestic manufacturing harder to maintain for others. Essentially, it comes down to the needs and goals of the company.

The Journal of Healthcare Contracting publisher John Pritchard recently sat down with several supply chain leaders to discuss the merits of investing in U.S.-based manufacturing for providers:

Rene Gurdian, Assistant Vice President of Supply Chain Finance and Strategy at Ochsner Health

George Godfrey, Chief Supply Chain Officer at Baptist Health South Florida

Bob Boswell, President and CEO at LeeSar & Cooperative Service of Florida

John Wood, CEO of Encompass

Changing sourcing strategies after COVID

Because of the pressures that COVID created for the healthcare supply chain, many organizations had to look for new sourcing strategies to improve supply chain assurance across the board. The biggest thing we learned from COVID is the lack of transparency and visibility around distribution and manufacturing, which led to the discovery of counterfeit products that did not meet the compliance standards required for their use in a healthcare setting. “We didn’t know where they were coming from. We didn’t know what types of challenges we were coming up against overseas,” Gurdian said.

At Ochsner, their Supply Chain leadership group has invested in several resiliency tools to better understand the bill of materials outside of the United States. This information provides their supply chain an improved transparent landscape that provides insight into the raw materials Ochsner is purchasing, which provides an opportunity to align long-term contingency plans on potential upcoming disruptions. Gurdian said, “At Ochsner, our overarching goal is to try to educate our team members, whether it’s a par technician or a contract analyst, that while [these individuals] are not at the beside directly, we are five to six degrees separated and we can potentially impact patient experience as well in tandem with the clinical experience.”

Patient care is of course the top priority, and that starts in places like supply closets. With the labor challenges facing healthcare within the nursing community, Gurdian used the example of hard-working nurses that need to spend time taking care of their patients, but that time is limited when they cannot locate the right products in the right place due to disheveled supply closets. “At Ochsner, we pride ourselves on the format of PAR closets (supply closets) and products being in a place that nurses can quickly locate the product and return to the bedside to be with their patients.”

Godfrey’s team at Baptist Health is among the many that have struggled with item substitutions in the last few years. These companies that struggled with item substitutions faced prices that increased as high as 200% for out-of-contract transactions. When organizations like Baptist Health are tied up in a contract that cannot procure the items they need, they have to source the items on an off-contract basis.

“Historically, supply chains don’t have the reporting capabilities to understand the complexities in item substitutions,” Godfrey said. “We go through contract renewals; we have a process in place. We understand increases and decreases, but when it comes to item substitution and you are in the hand-to-hand combat of getting supplies for the patients, the tools and analysis are not robust.”

The application of technology can be tricky when it comes to the human element of your organization. Automating your processes and applications after COVID might seem like an obvious choice to make, but it shouldn’t be at the expense of your team.

Godfrey said, “We look at technology not to replace people, but more to enable our people to do an outstanding job at what they are called to do. Whether it’s using technology for workload management or deploying supplies into one of the 1,100 supply cabinets we manage across 12 hospitals, we try to be innovative at everything we do. Additionally, if we are trying to drive success in certain areas, we are trying to measure success as we go along.”

Other organizations decided to improve their predictive analytics to improve their sourcing processes. At LeeSar, Boswell said through predictive analytics, they were able to leverage material resource planning capacity. He said, “We started leveraging more technology and freeing up our sourcing specialists and buyers to focus more on back orders. We also generate a daily pulse report that is a byproduct of our IT system. With this pulse report, we know the status of all inventory locations, current backorder and auto-sub status, raw and adjusted fill rates.”

Changing manufacturing processes after COVID

Sourcing strategies are among many things that have changed in the wake of COVID-19. If American manufacturing is going to be a viable option for providers going forward, there are things that need to change to make it more available for providers.

One of the biggest challenges facing domestic manufacturing is finding the people to fill these jobs. Labor costs and operational costs are higher for domestic manufacturing, but these costs can be offset with improved quality standards and smaller shipping windows.

For Encompass, John Wood and his team are considering shifting their manufacturing processes to nearshore instead of onshore.

“We have manufacturing in the U.S., but we have a big focus on moving to nearshore,” Wood said. “The mission for Encompass is really focused on the fact that we believe every patient, resident, caregiver, and family member needs to feel safe and comfortable in the healthcare environment. Safety is the biggest part of that, and the way we can assist people is by creating innovative products that are reliably delivered and cost effective.”

Nearshore sourcing allows for improved shipping windows from offshore sourcing. Wood said that a facility in China would have to guess what customers need three months in advance, but a nearshore facility in Mexico could drastically reduce that window.

From Wood’s perspective, COVID has forced his team to be better at what they do. “The big problem through COVID was the difference in lag time in the cost system. On the manufacturing side, we were getting price increases six months before.”

Wood believes whatever challenges that providers face in supply chain are due to “something in the chain that shouldn’t be there,” not because the healthcare industry is erratic. He said, “It’s complicated, right? You’ve got distributors, manufacturers, providers, GPOs. It’s become quite a complex system. I would say we do a better job with our direct IDNs because we have salespeople who go out and help us implement programs.”

The future of American manufacturing

Are we prepared for another pandemic? Another supply chain gridlock? What happens if another significant disruption upsets the balance again? The answer is complicated, but introducing more American manufacturing could be the key to avoiding some of the challenges that came from the coronavirus pandemic.

Gurdian said, “I think what we’ve learned is that there was a lack of transparency and education between the sales side of the suppliers to the supply chain side of the suppliers. I can sell products all day, but that doesn’t mean that I know how it’s made or where it comes from. What I’ve requested from any of the vendors that we talk to is to make sure that their team feels empowered to get some cross education with their peers in their organization within their organization’s supply chain department to really understand the products they are selling. It’s great to get a sale, but it’s not good if the product doesn’t show up.”

There’s of course a bit of give and take when it comes to engaging in domestic manufacturing. Onshoring manufacturing for healthcare companies will require higher labor and operational expenses, but it will also ensure the quality of the material and decrease shipping rates. Being able to visit the facilities for quality checks is a huge bonus for buyers, and it would have been a major advantage for healthcare organizations that were struggling with counterfeit products during the height of the pandemic. Ocean freight prices are astronomical, and it takes much longer for supplies to get in from an offshore source.

Another thing to consider for those looking to make a switch is the performance of their suppliers. Have you had difficulties in getting the supplies you needed? The quality of your supplier is a huge component to the success of your organization. “What we look at is supplier performance,” Godfrey said. “We are trying to move business away from the suppliers that do not manage their business very well.”

“At the end of the day, the most important thing is that patient care is not being compromised. Our first priority is to secure the supplies regardless of the source. In doing this there is a natural migration to the better performing and more consistent suppliers. Noble intentions are to support more domestic manufacturing and suppliers; the reality is that currently there are cost factors and limited supply in that space,” Boswell said.

CMS has proposed a 2.2 percent pay cut for home health providers next year, or an estimated $375 million less than 2023 levels.

Four things to know:

1. The proposed rule would increase payments to 2.7 percent, or $460 million, but home health agencies would see a 5.1 percent decrease that reflects the effects of the permanent behavior assumption adjustment (a $870 million decrease) and an estimated 0.2 percent increase for a proposed update to the fixed-dollar loss ratio used in determining outlier payments (a $35 million increase).

2. For 2024, using updated 2022 claims and the methodology finalized in the 2023 rule, CMS determined that it paid more under the new system than it would have under the old system. So, the agency is proposing an additional permanent adjustment percentage of -5.653 percent in 2024 to address the differences in the aggregate expenditures.

3. CMS is proposing to adopt two new measures for the home health quality reporting program in 2025, including a measure on the percentage of patients who are up to date with their COVID-19 vaccinations. The agency also proposed various changes to the measures used in the Home Health Value-based Purchasing program and the weighting methodology used to score performance and payment adjustments in the program.

4. The proposed rule is expected to be published in the Federal Register on July 10, with CMS accepting comments on the draft through Aug. 29.

Texas lawmakers have condemned a federal rule that could see the state lose about $8.4 billion in Medicaid funding, Allied News reported June 8.

A memo published by CMS in February aims to end payment agreements between Texas and hospitals in the state. Texas taxes hospitals to pay for Medicaid costs, and then gives hospitals funds it receives from the federal government to cover the incurred taxes, according to the report.

Texas hospitals also share their Medicaid funds to help hospitals that care for a higher proportion of low-income patients, but the federal memo targets this arrangement as illegal, according to NBC affiliate KXAN.

Texas is also the uninsured capital of the U.S., with more than 4.3 million Texans, 18.4 percent of residents, going without health insurance, according to the Texas Medical Association, which says state uninsurance rates — 1.75 times the national average — create significant problems in the financing and delivery of care.

“For 40 years, we’ve had a good system where the state and the federal government cooperate with healthcare providers to provide care,” Texas State Sen. Bryan Hughes said during a June 7 news conference. “But now, because of changes proposed by unelected bureaucrats, this whole system is in jeopardy.”

In April, states began disenrolling people from Medicaid after the expiration of a COVID-19 policy that allowed for continuous enrollment. As a result, an estimated 18 million people across the country will lose Medicaid coverage by June 2024, and 3.8 million of those will become uninsured, according to the Urban Institute and the Robert Wood Johnson Foundation. More than 1.2 million Texas are projected to be disenrolled over the next 12 months.

“CMS’ proposed rule would devastate the healthcare safety net at the expense of Texas’’ poorest residents, including low-income pregnant women, children and seniors,” John Hawkins, CEO of the Texas Hospital Association, told Becker’s. “Already navigating the challenge of carrying the nation’s highest rate of uninsured residents, Texas relies on its Medicaid program to make sure low-income Texans can access care in all corners of the state. This rule is the latest in a series of attacks on long-standing methods CMS has permitted states to use to finance their Medicaid programs. We are unclear why CMS has chosen to revive this position after it withdrew the roundly maligned Medicaid Fiscal Accountability Rule in early 2021.”

Texas Gov. Greg Abbott signed a bill into law June 13 aimed at improving patient safety by closing a longstanding loophole that allowed an infamous physician to keep practicing despite concerns of harm being done to patients, NBC affiliate KXAN reported.

The physician, nicknamed Dr. Death, was sentenced to life in prison in 2017 after being found guilty of harming or killing more than 30 patients. Despite concerns and because of gaps in reporting and monitoring in the National Practitioner Data Bank, he was allowed to continue practicing at multiple locations before his arrest.

The new bill, HB 1998, seeks to equip the Texas Medical Board with necessary tools to protect patients from dangerous physicians while also maintaining transparency about physician disciplinary records.

Here’s what else the new law will enforce:

Lying on medical license applications will be a Class A misdemeanor.

Physicians who have been convicted of a felony or misdemeanor related to moral turpitude are not allowed to practice medicine in the state.

Physicians who have had a medical license revoked, restricted or suspended in another state are not allowed to practice medicine in the state.

Monthly monitoring of physicians will be required using the National Practitioner Data Bank — which KXAN describes as “a confidential clearinghouse of all physician complaints, established by Congress.” The complaints are not publicly available.

The Texas Medical Board must update physician profiles on its website within 10 days of being notified about any disciplinary action against a physician.

Becker’s reached out to the Texas Medical Board for its comment on the passage of the legislation and will update this story if new information is provided.

Kaufman Hall analysis illustrates financial effects of inflation and the end of the COVID-19 public health emergency

CHICAGO – May 31ST, 2023 – Hospital finances broke even in April amid a continuing trend of high expenses and the unwinding of the Medicaid continuous coverage requirement of the COVID-19 public health emergency (PHE), according to the latest National Hospital Flash Report from Kaufman Hall.

Median YTD Operating Margin Shows Slight Improvement

The median year-to-date (YTD) operating margin index for hospitals was 0.0% in April, up slightly compared to -0.3% in March. With operating margins remaining at or below zero, hospitals have been left with little financial flexibility.

PHE Unwinding Begins

Hospitals experienced increases in bad debt and charity care in April. Combined with decreased patient volumes, Kaufman Hall experts note these data could illustrate the effects of the start of widespread disenrollment from Medicaid following the end of the PHE and the continuous enrollment provision that accompanied it. As states continue the process of redetermination, these trends will likely continue.

“With states conducting their Medicaid eligibility redetermination, it’s predicted that hundreds of thousands of people will ultimately become uninsured,” said Erik Swanson, senior vice president of Data and Analytics with Kaufman Hall. “The data indicate that we may already be seeing the effects of disenrollment materialize with patients less likely to seek out the care they need and a continued rise in bad debt and charity care.”

Inflation Pressures Hospital Finances

High expenses have been placing added strain on hospitals as they try to recover from the challenges of the pandemic. Labor expense per adjusted discharge increased 3% in April from March, and the costs of goods and services continued to be well above pre-pandemic levels. While total expenses fell slightly in April, operating revenues declined at a faster rate, down 5% month-over-month.

“Hospital and health system leaders must figure out how to navigate the new financial reality and begin to take action,” said Swanson. “In the face of operating margins that may never fully recover and inflated expenses, developing and executing a strategic path forward to a future that is financially sustainable is crucial.”

Kaufman Hallprovides management consulting solutions to help society’s foundational institutions realize sustained success amid changing market conditions. Since 1985, Kaufman Hall has been a trusted advisor to boards and executive management teams, helping them incorporate proven methods, rigorous analytics, and industry-leading solutions into their strategic planning and financial management processes, with a focus on achieving their most challenging goals.

Kaufman Hall services use a rigorous, disciplined, and structured approach that is based on the principles of corporate finance. The breadth and integration of Kaufman Hall advisory services are unparalleled, encompassing strategy; financial and capital planning; performance improvement; treasury and capital markets management; mergers, acquisitions, partnerships, and joint ventures; and real estate.

After three years of unprecedented challenges and caring for millions of patients, including over 6 million COVID-19 patients, America’s hospitals and health systems are facing a new existential challenge — sustained and significant increases in the costs required to care for patients and communities putting their financial stability at risk.

A confluence of several factors from historic inflation driving up the cost of medical supplies and equipment, to critical workforce shortages forcing hospitals to rely heavily on more expensive contract labor, led to 2022 being the most financially challenging year for hospitals since the pandemic began. Moreover, sustained demand for hospital care with patients coming to the hospital sicker and staying longer has exacerbated these challenges.

These challenges have been particularly financially devastating for hospitals and health systems because they come on top of two years of battling the COVID-19 pandemic. Hospitals and health systems have been on the front lines delivering care to patients, acting as de facto public health agencies, and incurring significant increases in costs from a range of inputs, including labor, drugs, supplies and administrative activities associated with burdensome billing and insurance tasks. In addition, as many individuals deferred care during the pandemic, hospitals saw a dramatic rise in patient acuity. At the same time, workforce shortages across the health care continuum have left hospitals unable to discharge patients to other care settings (e.g., skilled nursing facilities) creating patient bottlenecks with hospital beds occupied without any reimbursement.

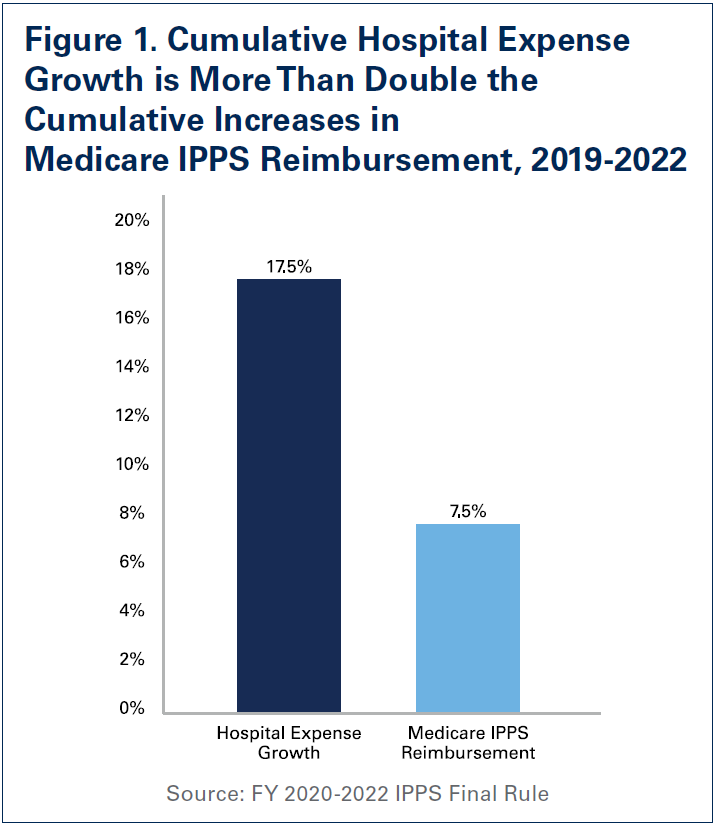

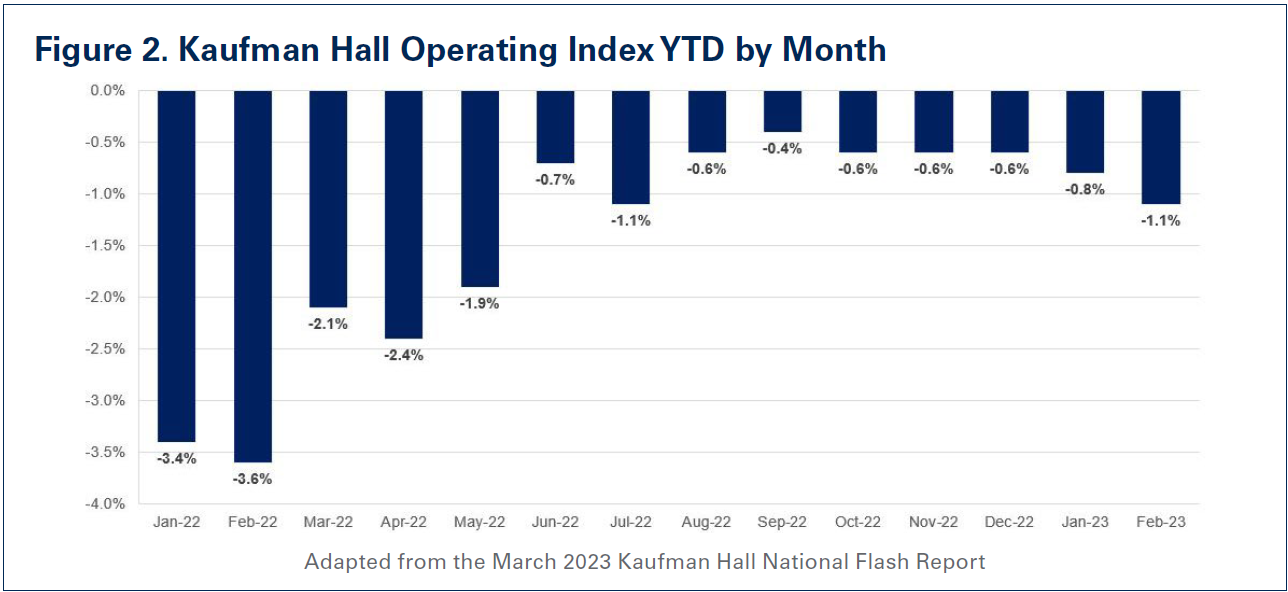

These unfortunate realities have resulted in a 17.5% increase in overall hospital expenses between 2019 and 2022, according to data from Syntellis Performance Solutions, a health care data and consulting firm. Further exacerbating the situation is the fact that the staggering expense increases have been met with woefully inadequate increases in government reimbursement. Specifically, hospital expense increases between 2019 and 2022 are more than double the increases in Medicare reimbursement for inpatient care during that same time (See Figure 1). Because of this, margins have remained consistently negative, according to Kaufman Hall’s Operating Margin Index throughout 2022 (See Figure 2). In fact, over half of hospitals ended 2022 operating at a financial loss — an unsustainable situation for any organization in any sector, let alone hospitals. So far, that trend has continued into 2023 with negative median operating margins in January and February. According to a recent analysis, the first quarter of 2023 saw the highest number of bond defaults among hospitals in over a decade.1 This also is one of the primary reasons that some hospitals, especially rural hospitals, have been forced to close their doors. Between 2010 and 2022, 143 rural hospitals closed — 19 of which occurred in 2020 alone.2,3 Finally, despite these cost increases, hospital prices have grown modestly. In fact, in 2022, growth in general inflation (8%) was more than double the growth in hospital prices (2.9%).

This report will examine the magnitude of cost increases over the last year, and the impact these increases have had on the financial stability of the hospital field.

Labor Expenses

Beginning in early 2022, the hospital field’s existing workforce shortages were exacerbated with increased patient demand for hospital care due to a combination of sustained COVID-19 surges, a new virulent disease affecting primarily pediatric patients called respiratory syncytial virus (RSV), and deferred care from the early days of the pandemic. To quickly meet this demand, hospitals were increasingly forced to turn to health care staffing agencies to fill necessary gaps, especially for bedside nursing and other critical allied health professionals such as respiratory and imaging technicians.

Labor has been really the primary driver of our increased expenses. We’ve seen a 17% increase in our nursing costs, for instance, during COVID, mainly because of many nurses leaving the field and the workforce. — President and CEO of a health system in the Northeast

A recent report by Syntellis Performance Solutions found that full-time equivalents (FTEs) for hospital contract employees jumped 138.5%. This reliance on temporary contract labor came at a significant expense to hospitals, as health care staffing agencies took advantage of the situation and increased their rates to record high levels. The same report found that the rate hospitals were charged for contract employees increased 56.8% in 2022 compared to pre-pandemic levels. It is for this reason that hospitals’ contract labor expenses increased a staggering 257.9% in 2022 relative to 2019 levels (See Figure 3).

The explosive growth in contract labor expenses in large part fueled the 20.8% increase in overall hospital labor expenses during the same time period. Even after accounting for the fact that patient acuity (as measured by the case mix index) has increased during this period, labor expenses per patient increased 24.7%. These increases are particularly challenging, because labor on average accounts for about half of a hospital’s budget.

Non-Labor Expenses

The historic rise in inflation has been particularly challenging for hospitals and health systems as it has sparked a significant increase in non-labor expenses. As prices for essential goods such as food and clothing have seen significant price growth, so too have the prices for essential goods for hospitals such as drugs and medical supplies.4 A report by Kaufman Hall estimated that non-labor expenses alone would result in a one-year expense increase of $49 billion for hospitals and health systems.5,6 In fact, since 2019, non-labor expenses have increased 16.6% on a per patient basis. Below, we focus on three areas of non-labor expenses that have seen tremendous cost growth:

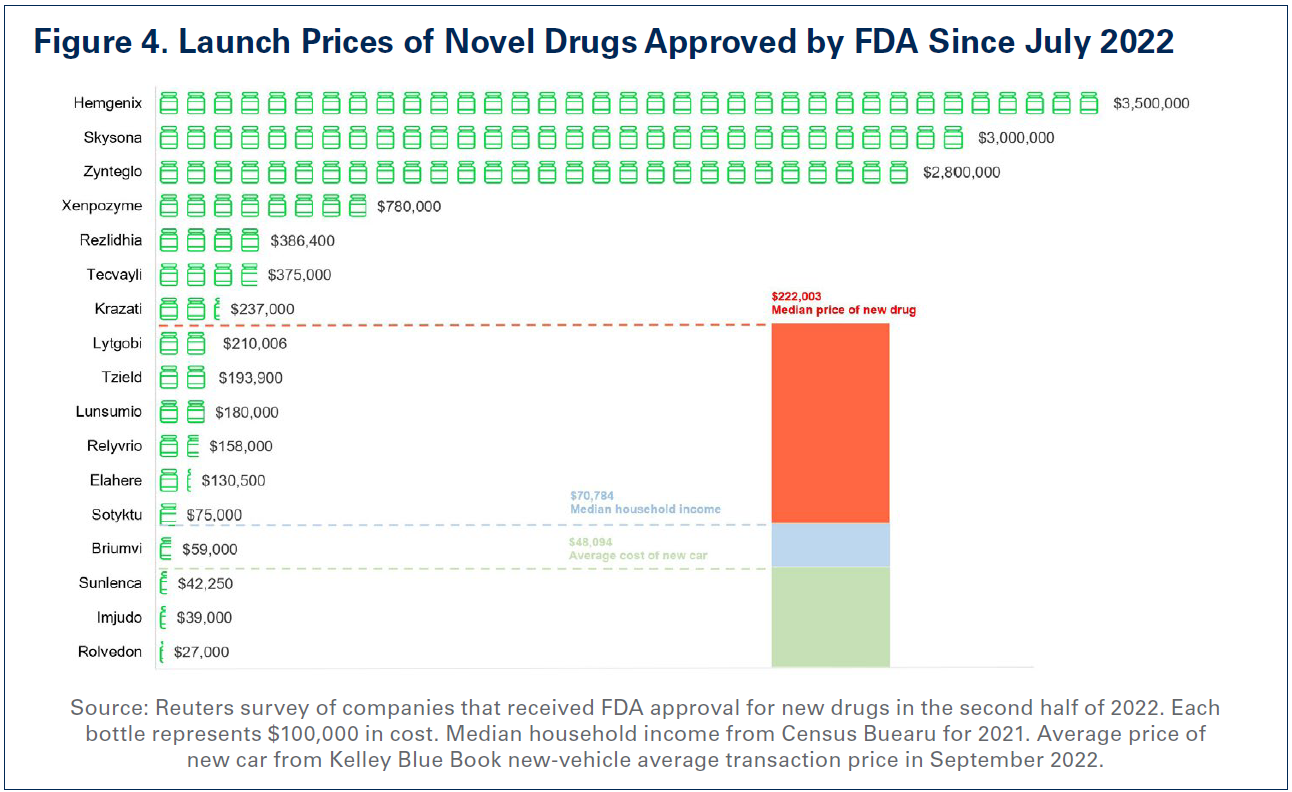

As hospitals and health systems faced an increasingly challenging environment due to pandemic surges as well as workforce shortages, drug companies took the opportunity to significantly raise the prices of existing drugs as well as introduce new drugs at record prices.7 High drug prices affect both patients directly and hospitals, especially when purchasing provider-administered drugs. In fact, for the first time in history, the median price of a new drug exceeded $200,000 — a staggering figure that implies a double-digit year-over-year price growth (See Figure 4).8,9 To further contextualize these launch prices, the median new drug launch price is more than quadruple the average price of a new car and more than triple the median annual household salary ($70,784) in the United States, illustrating how unaffordable these drugs are for both providers and their patients.10

In addition, a report by the Assistant Secretary for Planning & Evaluation (ASPE) at the Department of Health and Human Services (HHS) found that drug companies increased drug prices for 1,216 drugs — many used to treat chronic conditions like cancer and rheumatoid arthritis — by more than the rate of inflation, which was 8.5% between 2021 and 2022. In fact, the average price increase for these drugs was 31.6%, with some drugs experiencing price increases as much as 500%.11 Moreover, recent drug shortages, specifically for certain drugs used to treat cancer, have also fueled further expense growth. It is estimated that drug shortages alone cost hospitals nearly $360 million a year.12

Therefore, it is no surprise, that as hospitals face the reality of operating on negative margins, drug companies are enjoying record revenues and profits. For example, some drug companies are experiencing over 200% revenue growth.13

“In the last year, we’ve seen double digit increases in pharmaceuticals and medical supplies. Our utility costs are up and certainly our labor costs are up.” — CEO of a health system in the South

For these reasons, high drug prices have been a primary driver of skyrocketing drug costs for hospitals. According to data from Syntellis Performance Solutions, hospital drug expenses per patient have increased 19.7% between 2019 and 2022. Even after accounting for the fact that patients were on average sicker (as measured by the case mix index) in 2022 than in 2019, drug expenses per patient were up over 18%. This suggests that the growth in hospital drug expenses is not primarily due to sicker patients requiring more drugs, rather it is a result of drug companies’ deliberate decisions to increase the prices of their products.

II. Medical Supplies and Equipment

While the demand for patient care has risen, so has the need for medical supplies necessary to deliver patient care and personal protective equipment (PPE) necessary to ensure the safety of both hospital staff and patients. Hospitals rely on a global supply chain for access to these supplies and equipment, and entities across the supply chain have experienced inflationary cost increases. Ongoing supply chain disruptions have led to higher manufacturing costs, packaging costs, and shipping costs, which translate into higher prices for hospitals.14 In fact, the National Academies recently released a report highlighting the ongoing challenges that supply chain disruptions place on providers needing to access medical supplies.15

“But in other industries like we see in our area, manufacturing, retail, hospitality, you can decide not to fill that order. You can decide to shut your restaurant down for a day. We can’t do that in health care.” — President and CEO of a health system in the Midwest

As a direct result, hospital supply expenses per patient increased 18.5% between 2019 and 2022, outpacing increases in inflation by nearly 30%. Particularly alarming is the growth in supply costs needed for care in the emergency department — often the first level of care provided in the hospital. Hospital expenses for emergency services supplies experienced a nearly 33% increase between 2019 and 2022. These include equipment such as ventilators, respirators and other sophisticated equipment that are critical to keeping patients alive in the emergency department. As patient acuity has increased dramatically during this period, the need for these equipment to care for more complex patients also has increased.16 More specifically, as patients stay in the hospital longer requiring more intensive care, the amount of supplies and the type of supplies required to care for those patients become more expensive.17

III. Other Non-Labor Expenses

In addition to hospitals’ costs for drugs and medical supplies and equipment, costs for other areas that help support patient care such as purchased service expenses also have risen precipitously. This, in part, has driven clinical costs higher, making clinical services such as emergency and lab services more expensive to administer.

Purchased service expenses, which are expenses hospitals incur to create operational efficiencies such as information technology (IT), environmental services and facilities, and food and nutrition services increased 18% between 2019 and 2022. With increased patient demand and inflationary pressures, hospitals have been forced to incur additional purchased service costs as they renew and renegotiate their purchased service contracts. For example, as the cost of food has gone up over the last year, hospitals’ food services costs have grown. Specifically, food and nutrition service expenses per patient grew over 15% between 2019 and 2022.

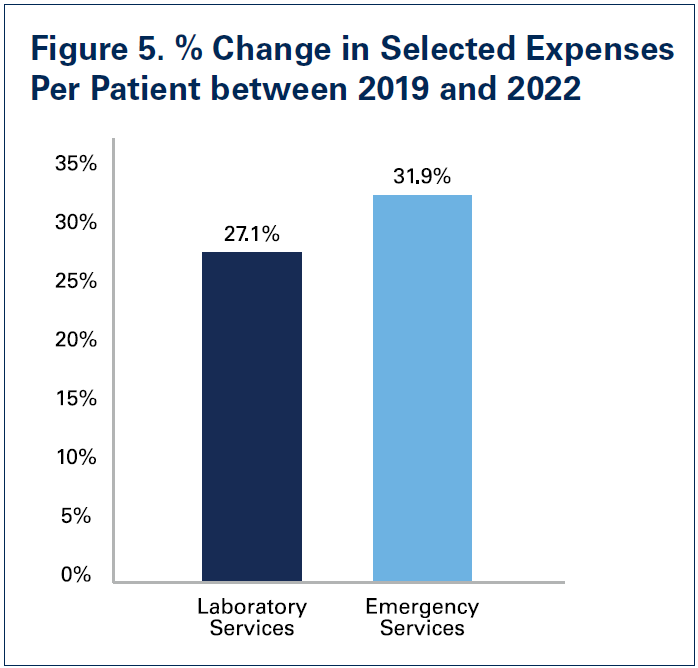

Hospitals also have incurred increased costs in particular clinical areas. This is due to a combination of increased patient demand after many patients delayed or avoided care during the pandemic and inflationary cost growth for supplies and equipment needed to provide care. Specifically, compared to 2019 levels, laboratory service expenses per patient were up 27.1% in 2022 and emergency service expenses per patient were up 31.9%.

With hospitals bearing cost growth in many areas, they have been forced to cut costs elsewhere to stay financially afloat, and in the case of many rural hospitals, simply keep the doors open.

Expenses from Burdensome Insurer Policies

Notwithstanding labor and non-labor expense increases, commercial health insurer policies like unnecessary prior authorization requirements and improper claim denials continue to add significant burden for hospital staff — diverting staff time from caring for patients and contributing to clinician burnout. These practices add substantial administrative costs to the health care system by slowing down the provision of care, requiring providers to purchase additional IT tools to manage insurer requirements and necessitating the hiring of additional staff solely to manage administrative paperwork.

Administrative costs constitute as much as 31% of total health care spending — 82% of which can be attributed to billing and insurance.18 In a recent survey fielded by the AHA, 84% of hospitals reported the cost of complying with insurer policies is increasing, with 95% reporting increases in time spent seeking prior authorization approval.19 Even though more than half of all prior authorization denials are overturned, commercial health insurers continue to flood hospitals with prior authorization denials to the detriment of both patients and providers. This is especially egregious when prior authorization is required for widely available lifesaving medications with clear clinical indications for use, such as insulin, where the service or treatment protocol are neither new nor have a history of unwarranted variation in utilization. The AHA report also found that 50% of hospitals and health systems have more than $100 million in accounts receivables for claims that are older than six months, which impact hospitals’ cash flow and ability to weather the avalanche of cost increases they have faced. Shockingly, seven in 10 hospitals reported having an outstanding claim from 2016 or older. In addition, 35% of hospitals reported $50 million or more in foregone payments because of denied claims.

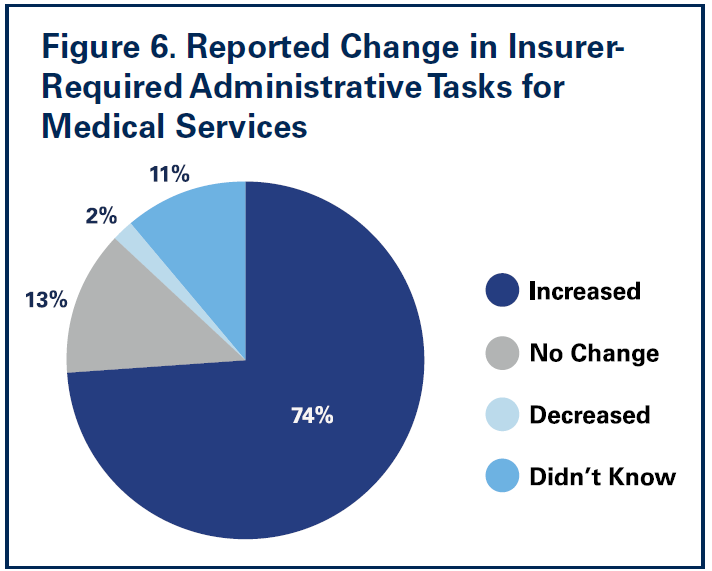

A recent survey conducted by Morning Consult on behalf of the AHA found that nearly three-fourths of nurses reported increases in insurer-required administrative tasks for medical services over the last five years. Nearly 9 in 10 nurses reported insurer administrative burden had negatively impacted patient clinical outcomes (See Figure 6 on next page).

Confronted by ever-growing costs, hospitals have been limited in how they can respond to the administrative burden levied by commercial health plans. Over the course of the last several years many hospitals, looking for operational efficiencies to combat rising costs, have been driven to trim down their administrative workforce.20 However, with a narrowing menu of options for hospitals to choose from in responding to insurer administrative expenses, 78% of hospitals report their experience with commercial health insurers is getting worse.

Outlook for the Rest of 2023

As the public health emergency comes to end on May 11, a number of important waivers and flexibilities also will come to an end immediately, or will sunset at the end of this year.21 The downstream effects of this will be wide-ranging as hospitals will be faced with a set of additional challenges. For example, with the end of the public health emergency, the continuous Medicaid enrollment provision will no longer be in effect starting April 1 meaning that states can begin dis-enrolling current Medicaid beneficiaries from the program that do not meet the state’s Medicaid enrollment criteria. According to the Kaiser Family Foundation, as many as 14 million current Medicaid beneficiaries could lose coverage over the next year.22 Undoubtedly, these coverage losses will drive higher rates of uninsured and underinsured individuals, raising hospitals’ uncompensated care costs and potentially negatively impacting disproportionate share payments as well as 340B program eligibility, both of which allow hospitals to offset some of the expense increases as well as furnish programs and services critical to patients. Further, the ending of regulatory relief through the 20% Medicare inpatient prospective payment system add-on payment for beneficiaries diagnosed with COVID-19 to offset the cost of highly complex care for these patients, will certainly add financial pressure to an already fragile situation for hospitals and health systems.

The combination of the impacts on hospitals of the ending public health emergency as well as continued expense growth has created an uncertain future for hospitals and health systems. A study by McKinsey on the impact of inflation and other cost pressures for the health care system projected that there would be $98 billion in additional costs between 2022 and 2023 alone, representing an astounding $248 billion increase in costs relative to 2019.23 In fact, their projections suggest that non-labor costs alone could increase by $112 billion by 2027. Therefore, it is no surprise, that credit rating agencies have a negative outlook for the field. For example, Moody’s has projected a negative outlook for the hospital field for 2023 due in large part to inflationary cost pressures and persisting workforce challenges.24

Conclusion

Hospitals and health systems — and their teams — are committed to providing high-quality care to all patients in every community. This steadfast commitment to caring and advancing health has never been more apparent than during the last three years battling the greatest public health crisis in a century.

However, the costs of delivering on this commitment to care have grown tremendously. As the data in this report show, 2022 brought an unprecedented set of challenges for hospitals and health systems, which has left the field in a financially unsustainable situation. These challenges are continuing in 2023.

To address these challenges and ensure hospitals have the ability to continue taking care of the sick and injured, as well as keeping people and communities healthy, congressional support and action are necessary. Among other actions, Congress should:

enact policies that bolster hospitals and health systems’ efforts to support today’s workforce and ensure a future pipeline of professionals to mitigate longstanding workforce challenges and meet the nation’s increasing demands for care;

reject efforts to cut any Medicare or Medicaid payments to hospitals and health systems. Medicare and Medicaid significantly underpay the costs of providing care and further cuts could reduce access to care for patients and communities;

establish a temporary per diem payment to address a backlog in hospital patient discharges due to workforce shortages;

urge the Centers for Medicare & Medicaid Services to use its “special exceptions and adjustments” authority to make a retrospective adjustment to account for the difference between the market basket update that was implemented for fiscal year (FY) 2022 and what the market basket is currently projected to be for FY 2022; and

create a special statutory designation and provide additional support for metropolitan anchor hospitals that serve historically marginalized communities.

As the hospital field maintains its commitment to care in the face of significant challenges, policymakers must step up and help protect the health and well-being of our nation by ensuring America has strong hospitals and health systems.

The American Hospital Association released a report in April examining the costs that drove 2022 to be a financial low point for hospitals and health systems.

The AHA’s “Cost of Caring” report contains percent changes for a number of expense categories from 2019 to 2022, with data from consulting firm Syntellis Performance Solutions. It concludes with five suggestions from the association to Congress for action and greater support, including the rejection of any efforts to cut Medicare and Medicaid reimbursement.

“Rising costs for drugs, supplies, and labor coupled with sicker patients, longer hospital stays and government reimbursement rates that do not come close to covering the costs of caring for patients have created a dire situation for hospitals and health systems,” AHA President and CEO Rick Pollack said in the report. “This is not just a financial problem, it is an access problem. When healthcare providers cannot afford the tools and teams they need to care for patients, they will be forced to make hard choices and the people who will be impacted the most are patients. We can’t let that happen. Congress and others must act to preserve the care our nation needs and depends on.”

Below are some key figures from the report, which can be found in full here.

1. Overall hospital expenses increased by 17.5 percent from 2019 to 2022, according to data from consulting firm Syntellis Performance Solutions. By comparison, Medicare reimbursement increased 7.5 percent in the same timeframe.

2. Overall hospital labor expenses increased 20.8 percent from 2019 to 2022, with labor expenses per patient up 24.7 percent.

3. Temporary contract labor was a significant expense within the labor category throughout the COVID-19 pandemic. Total contract labor expenses for hospitals in 2022 were 258 percent higher than in 2019. The rate hospitals were charged for contract employees increased 56.8 percent in 2022 compared to pre-pandemic levels.

4. Drugs make up another large expense category for hospitals, which have seen a 19.7 percent increase in drug expenses per patient between 2019 and 2022. This measure exceeds 18 percent when accounting for patient case mix and acuity, suggesting the increase stems from drugmakers’ pricing strategies.

5. Purchased service expenses — for operational functions such as IT, environmental services and facilities, and food and nutrition services — increased 18 percent between 2019 and 2022.

6. Hospital supply expenses per patient increased 18.5 percent between 2019 and 2022. Emergency departments were especially hard-hit by supply costs, which grew 33 percent between 2019 and 2022.

7. Food and nutrition service expenses per patient increased 15 percent between 2019 and 2022.

8. Laboratory service expenses per patient increased 27.1 percent between 2019 and 2022. Emergency service expenses per patient grew 31.9 percent in the same timeframe.

These challenges have been particularly financially devastating for hospitals and health systems because they come on top of two years of battling the COVID-19 pandemic. Hospitals and health systems have been on the front lines delivering care to patients, acting as de facto public health agencies, and incurring significant increases in costs from a range of inputs, including labor, drugs, supplies and administrative activities associated with burdensome billing and insurance tasks. In addition, as many individuals deferred care during the pandemic, hospitals saw a dramatic rise in patient acuity. At the same time, workforce shortages across the health care continuum have left hospitals unable to discharge patients to other care settings (e.g., skilled nursing facilities) creating patient bottlenecks with hospital beds occupied without any reimbursement.

These challenges have been particularly financially devastating for hospitals and health systems because they come on top of two years of battling the COVID-19 pandemic. Hospitals and health systems have been on the front lines delivering care to patients, acting as de facto public health agencies, and incurring significant increases in costs from a range of inputs, including labor, drugs, supplies and administrative activities associated with burdensome billing and insurance tasks. In addition, as many individuals deferred care during the pandemic, hospitals saw a dramatic rise in patient acuity. At the same time, workforce shortages across the health care continuum have left hospitals unable to discharge patients to other care settings (e.g., skilled nursing facilities) creating patient bottlenecks with hospital beds occupied without any reimbursement.

In addition to hospitals’ costs for drugs and medical supplies and equipment, costs for other areas that help support patient care such as purchased service expenses also have risen precipitously. This, in part, has driven clinical costs higher, making clinical services such as emergency and lab services more expensive to administer.

In addition to hospitals’ costs for drugs and medical supplies and equipment, costs for other areas that help support patient care such as purchased service expenses also have risen precipitously. This, in part, has driven clinical costs higher, making clinical services such as emergency and lab services more expensive to administer. A recent survey conducted by Morning Consult on behalf of the AHA found that nearly three-fourths of nurses reported increases in insurer-required administrative tasks for medical services over the last five years. Nearly 9 in 10 nurses reported insurer administrative burden had negatively impacted patient clinical outcomes (See

A recent survey conducted by Morning Consult on behalf of the AHA found that nearly three-fourths of nurses reported increases in insurer-required administrative tasks for medical services over the last five years. Nearly 9 in 10 nurses reported insurer administrative burden had negatively impacted patient clinical outcomes (See